Canadian credit spreads have moved wider in recent weeks, raising understandable questions about the market outlook. While the change reflects a more cautious backdrop, today’s spread levels remain far below those associated with past periods of acute credit stress. This paper examines the recent move in context and considers what it may mean for investors.

The latest period of geopolitical uncertainty has impacted many areas of financial markets, and Canadian credit markets have not been immune. We are beginning to see early signs of softening.

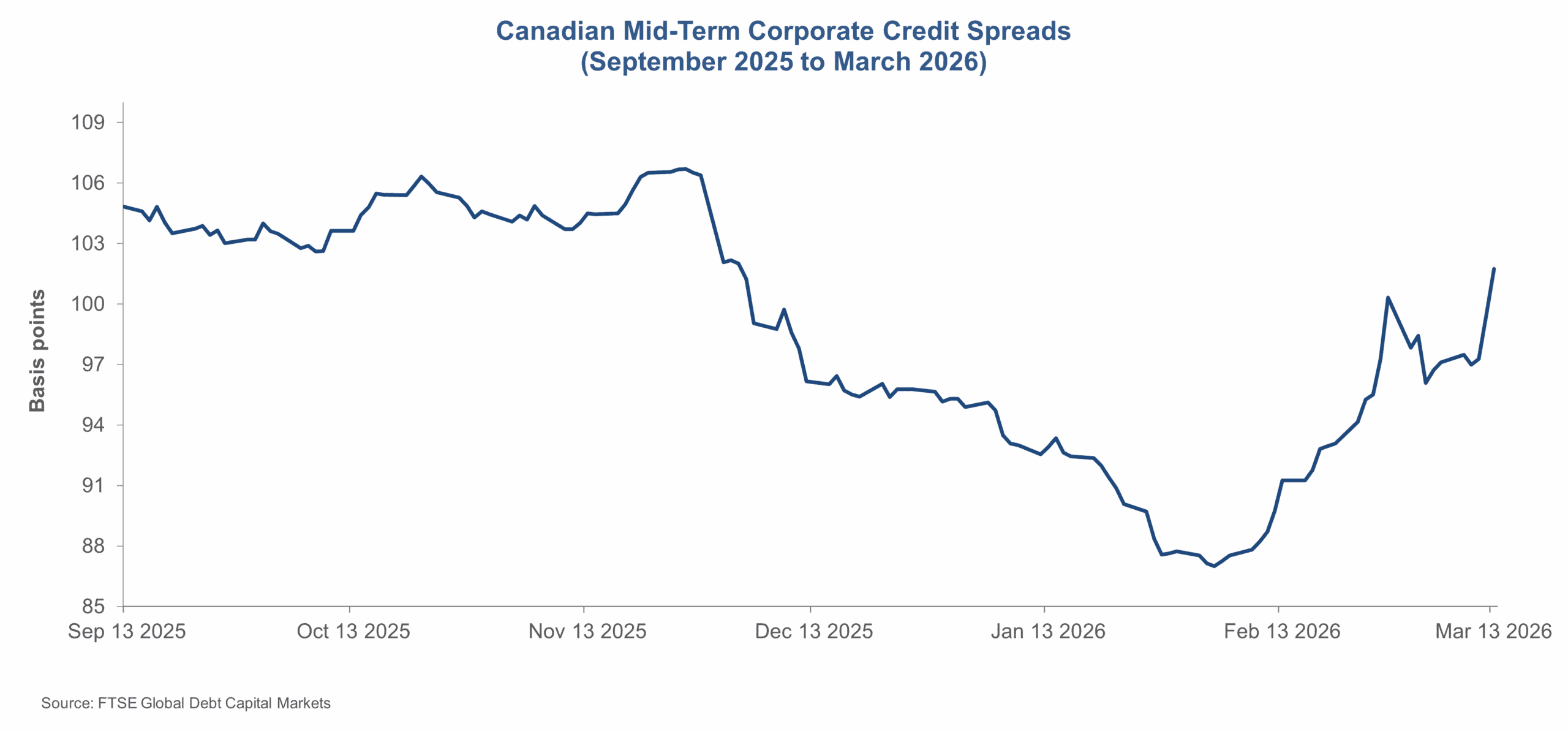

After an extended period of stability and tightening, credit spreads have started to move modestly wider, broadly mirroring moves seen in other risk assets. Over shorter time horizons, such as the six-month period shown below, the widening is noticeable.

As geopolitical tensions and broader macro uncertainty have increased, investors have begun to demand higher compensation for accepting greater credit risk in their portfolios. In this environment, market liquidity can become more fragile, with dealer balance sheets less willing to intermediate risk and investors becoming more selective in deploying capital. As a result, even relatively modest selling pressure can lead to a more noticeable adjustment in spreads. The recent widening appears consistent with investors rebuilding a more typical risk premium across credit markets.

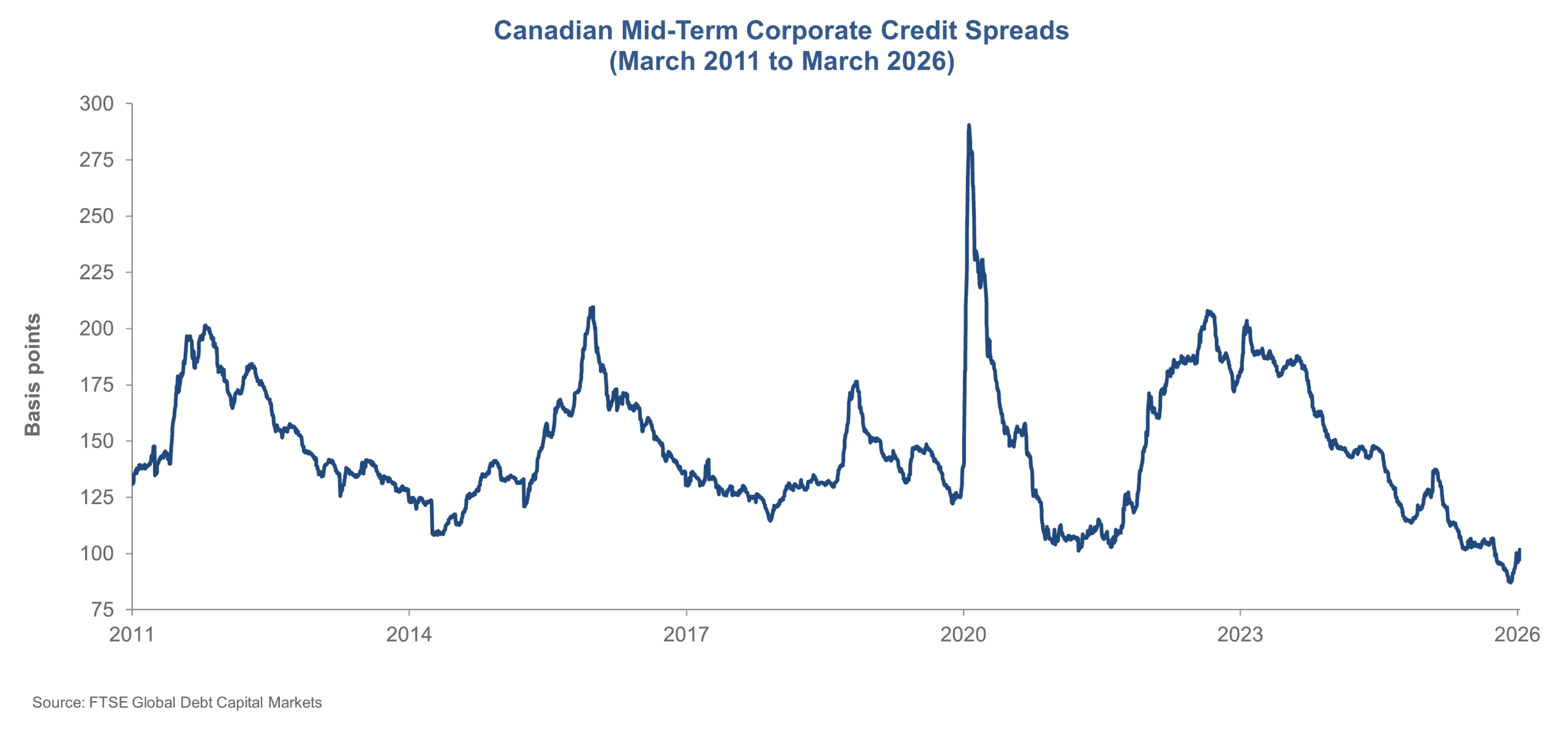

Placing the recent past in a longer-term context, as seen in the chart below, provides a more balanced perspective. Even after the widening of the last few weeks, credit spreads remain well below the elevated levels observed during previous periods of market stress. Over the past several years, spreads have moved through multiple cycles – widening during risk-off environments and tightening as financial conditions improved.

Viewed through that lens, the recent increase appears modest relative to historical episodes and, at least for now, more reflective of a market recalibrating expectations than a broad deterioration in credit fundamentals.

At the same time, the broader rate environment continues to shape investor behaviour. Government of Canada yields remain elevated relative to the ultra-low-rate environment that prevailed for much of the previous 15 years. As a result, even with spreads beginning to widen, the all-in yield available on corporate bonds remains attractive, continuing to draw investor demand and helping to moderate the move in spreads.

We remain cautious and expect volatility to remain a persistent feature of the markets. We will continue to focus on downside protection and disciplined positioning while selectively pursuing new opportunities.

This material is intended for information purposes only and does not constitute legal, tax, securities or investment advice, an opinion regarding the suitability of any investment nor a solicitation of any type. The opinions expressed are as of March 2026 and are subject to change without notice.